After completing this chapter, you will be able to:

Classify missing data mechanisms (MCAR, MAR, MNAR) and understand when each is ignorable for inference.

Recognize and quantify biases from missing data, including survivorship bias, instant history bias, and selection bias.

Apply appropriate techniques for handling missing data (complete case analysis, imputation, weighting, model-based procedures).

Implement multiple imputation workflows and understand their assumptions and uncertainty.

Critically evaluate claims based on incomplete data and perform sensitivity analyses.

Note

This chapter addresses a ubiquitous problem in real-world data analysis: missing data. We’ll see through concrete examples how missing data can severely bias results, learn to classify different mechanisms that generate missingness, and explore practical methods for dealing with incomplete data. The material is enriched with findings from Fung and Hsieh (2000) and Karvanen et al. (2016).

12.2 Introduction: The Hidden Cost of Missing Data

Missing data are ubiquitous in real-world applications. They are caused by limitations and defects of sensors, people failing to respond to surveys, entities disappearing in the middle of a long-term study, and countless other reasons.

Data that are missing randomly are often benign: the law of large numbers and the central limit theorem help manage their impact. But data that are missing systematically can be a serious problem, as the following examples will demonstrate.

12.2.1 Opening Example: Investment Fund Performance

Consider three hypothetical investment funds, all established simultaneously and investing in risky assets. After 3 years:

Fund A has done well, reaching an average annual return of 10%

Fund B has done OK, reaching an average annual return of 5%

Fund C has been terrible, making an average annual loss of -3%

It is unlikely that investors would stick with Fund C, so it is likely to have made a quiet exit – for example, by returning the funds to investors and liquidating.

Question: What is the average performance of the funds?

Looking at surviving funds only: (10 + 5)/2 = 7.5% per year

Looking at all funds that started: (10 + 5 - 3)/3 = 4% per year

The difference – a seemingly small 3.5 percentage points – is an example of survivorship bias. Over time, this translates to millions in misallocated capital if investors rely on biased performance data.

Survivorship Bias is Everywhere

Survivorship bias happens everywhere entities in a long-term study can selectively disappear:

Subjects in long-term medication or diet studies who drop out

Individuals who have reached success or fame (we don’t see those who tried and failed)

Companies that went bankrupt and were removed from stock indices

Startups that shut down before being included in databases

12.2.2 A Historical Example: The Bomber Plane Problem

You probably have heard this story: during World War II, the U.S. military analyzed damage patterns on bomber planes returning from missions to decide where to add armor.

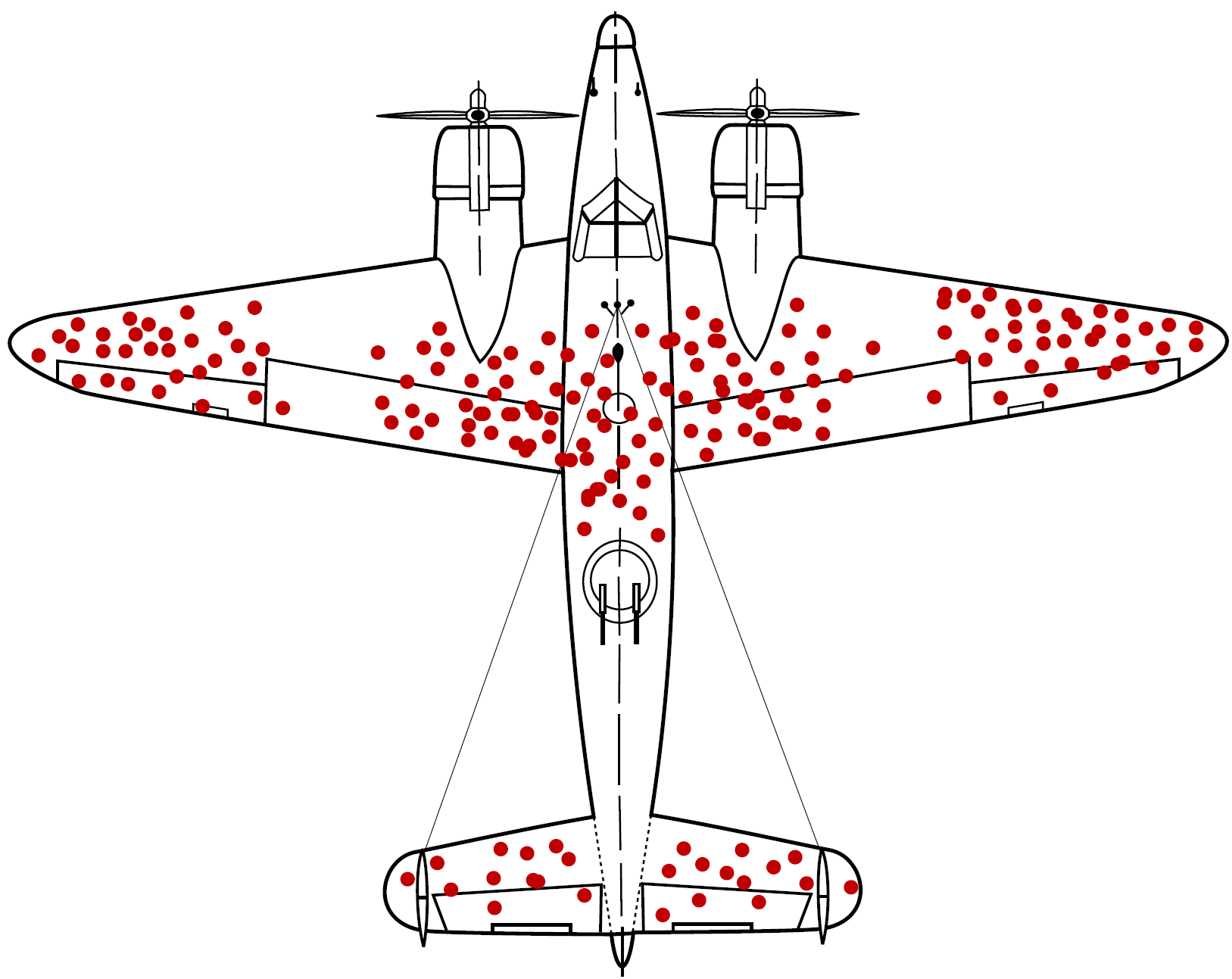

Survivorship bias illustrated: bullet hole patterns on returning aircraft. The red areas show where returning planes were hit. Figure by Martin Grandjean (vector), McGeddon (picture), Cameron Moll (concept); CC BY-SA 4.0.

The intuitive approach would be to reinforce the areas with the most bullet holes – after all, those are clearly getting hit frequently. Instead, statistician Abraham Wald made a crucial observation: the data showed where planes could take damage and still return. The planes that were hit in other locations didn’t make it back and weren’t in the dataset.

According to this insight, engineers should reinforce the areas without bullet holes. Those were the critical spots where damage meant the plane never returned. This is a classic example of selection bias in missing data – the missing observations (planes that didn’t return) contained the most important information.

Finnish Terminology Reference

For Finnish-speaking students, here’s a reference table of key terms:

English

Finnish

Missing data

Puuttuva tieto / Puuttuvat havainnot

Survivorship bias

Selviytymisharha

Selection bias

Valikoitumisharha / Valintaharha

Instant history bias

Takautuvan historian harha

Missing completely at random (MCAR)

Täysin satunnaisesti puuttuva

Missing at random (MAR)

Satunnaisesti puuttuva

Missing not at random (MNAR)

Ei-satunnaisesti puuttuva

Ignorable

Sivuutettava

Imputation

Imputaatio / Puuttuvien arvojen korvaaminen

Multiple imputation

Moninkertainen imputointi

Censoring

Sensurointi

Complete case analysis

Täydellisten havaintojen analyysi

12.3 Case Studies: When Missing Data Misleads

12.3.1 Financial Performance Biases

All standard financial indices are susceptible to survivorship bias: unsuccessful companies and funds are regularly removed and replaced by more successful competitors.

The issue is made worse by instant history bias: when successful funds are added to a database, their historical returns from their incubation period are backfilled, but only the winners make it to the database.

Observed Hedge Fund Performance Biases

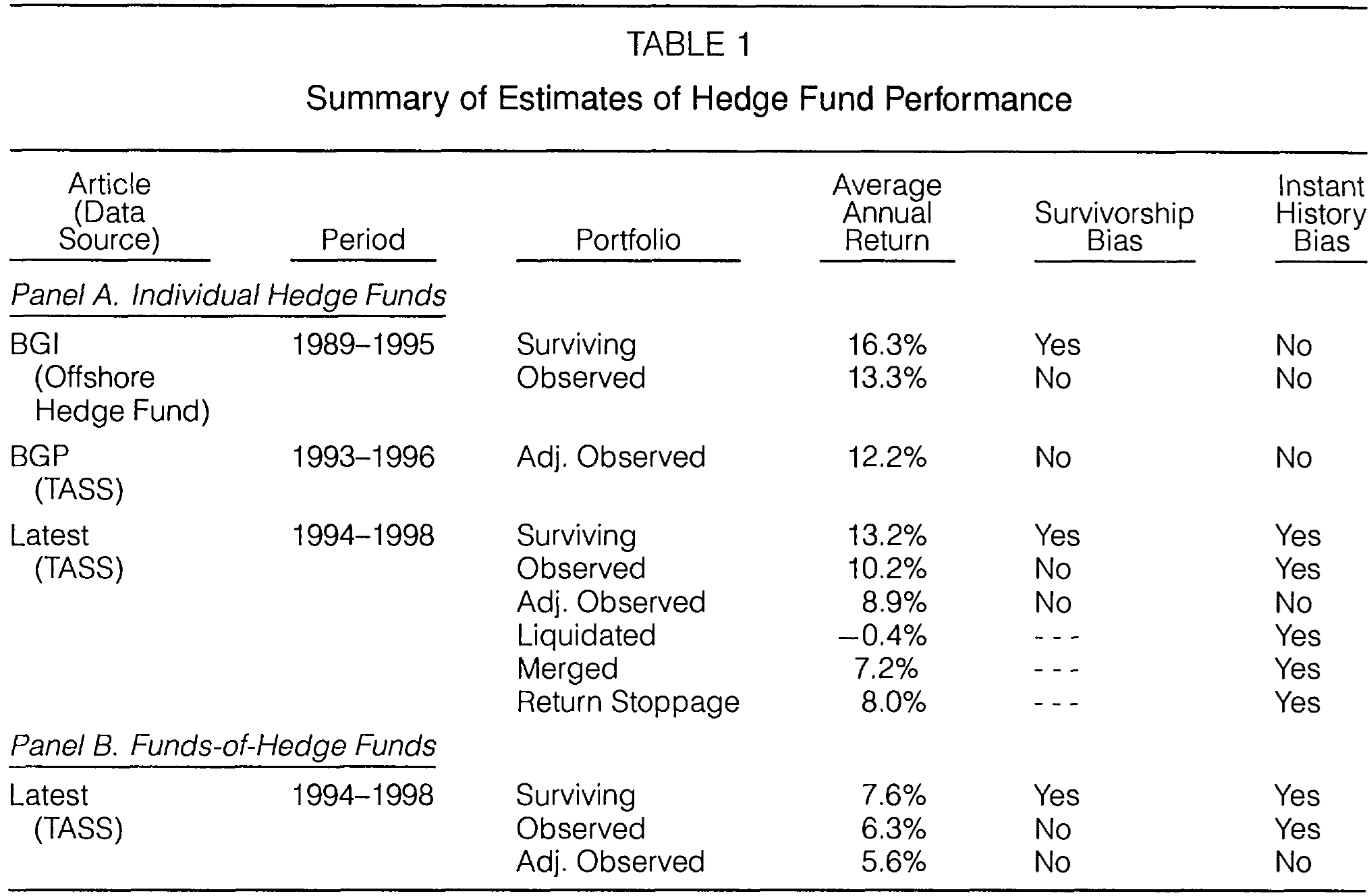

Fung and Hsieh (2000) provide quantitative estimates of these biases using hedge fund data:

Survivorship and instant history bias in hedge fund performance data. The table shows estimates from the TASS database for both hedge funds and commodity trading advisors (CTAs). Figure from Fung and Hsieh (2000).

Key findings:

Survivorship bias in hedge fund performance estimates: approximately 3% per year

Instant history bias: around 1.4% per year for hedge funds, 3.6% per year for CTAs

Dropout rates: About 20% per year for offshore hedge funds, 19% per year for CTAs

Further bias is caused by selection bias, where fund managers can decide whether to include their fund in the indices, with better-performing funds more likely to be included.

The Funds-of-Funds Solution

One way to understand the true bias is to track an investment in a “fund of funds” that invests in every fund in the market. The track records of funds-of-funds:

Retain the investment experience of hedge funds that went out of business due to poor performance

Include hedge funds that stopped reporting to database vendors because of good performance

Don’t suffer from instant history bias (past records are unaffected when adding new funds)

Fung and Hsieh (2000) use this approach to validate their bias estimates, finding that adjusted individual fund returns align well with funds-of-funds returns after accounting for portfolio management costs.

Types of Bias in Fund Data

Let’s break down the different biases more carefully:

Survivorship Bias: Failed funds disappear from databases. Studies comparing surviving funds to all funds (including defunct ones) consistently show that surviving funds have higher average returns – not because they’re better, but because the worst performers are missing from the data.

Instant History Bias: New hedge funds typically undergo an incubation period, trading on money from the managers’ friends and relatives. After compiling good performance, they market themselves to database vendors and hedge fund consultants. When vendors add these funds to their databases, they backfill the earlier returns during the incubation period. The median incubation period for hedge funds is about 343 days (roughly 11 months), during which only the successful funds survive to be added.

Selection Bias: Only funds with good performance want to be included in a database. However, this effect is somewhat mitigated because some managers with superior performance deliberately don’t participate – particularly when they’re not interested in attracting more capital.

Advanced: Multi-Period Sampling Bias

Many databases require funds to have a minimum track record (e.g., 24–36 months) before inclusion. This creates an additional upward bias: funds that survive the initial period tend to have better performance than those that failed early.

Fung and Hsieh (2000) quantify this multi-period sampling bias:

Hedge funds: Approximately +0.6% per year

Commodity trading advisors (CTAs): Approximately +0.1% per year

Practical implication: When constructing performance indices or conducting research, one should apply bias adjustments before imposing minimum history requirements. Otherwise, they would compound the survivorship bias with this additional selection effect.

12.3.2 Missing Responses in Health Surveys

Our second major example comes from population health surveillance. The FINRISK 2007 study investigated whether survey participants accurately represent the full population.

The FINRISK 2007 Study Design

In the 2007 study, a random sample of 10,000 individuals aged 25–74 were invited to participate in a health examination survey in Finland:

Both participants and non-participants were followed up for deaths and hospitalizations for 5 years

However, the participants did not appear to fully represent the study population. The full population had substantially higher death rates:

Estimates of health indicators for different participation groups.

Subset

Heavy alcohol users % (95% CI)

Daily smokers % (95% CI)

BMI ≥ 30 kg/m² % (95% CI)

Systolic blood pressure ≥ 140 mm Hg % (95% CI)

Deaths per 1,000 (95% CI)

Hospitalizations per 1,000 (95% CI)

Full cohort

—

—

—

—

33.0 (29.5–36.5)

1,157 (1,098–1,215)

Participants

5.2 (4.7–5.8)

21.8 (20.7–22.8)

21.0 (20.0–22.0)

30.7 (29.5–31.8)

22.1 (18.5–25.7)

1,052 (989–1,115)

A subset of health indicators by participation group. Participants and non-participants show markedly different mortality and hospitalization patterns (bolded). Data from Table 5 of Karvanen et al. (2016).

This raises serious questions about the validity of health indicators estimated using only the survey respondents.

Estimating Health Indicators Without Ground Truth

The primary goal of the FINRISK study was to estimate population-level prevalences of key health indicators:

Heavy alcohol use (self-reported questionnaire data)

Daily smoking (self-reported questionnaire data)

Obesity (BMI \geq 30 kg/m^2, measured)

High blood pressure (systolic BP \geq 140 mm Hg, measured)

Elevated total cholesterol (\geq 5.0 mmol/L, measured)

These variables are only available for study participants. We have no direct way to measure smoking or alcohol use for the 37% who didn’t participate. We cannot simply use participant-only estimates because, as the mortality data shows, non-participants are fundamentally different from participants.

While we don’t have ground truth for health behaviors among non-participants, we do have complete data on deaths and hospitalizations for everyone – both participants and non-participants. These follow-up outcomes provide a rare opportunity to validate different statistical methods by checking whether they recover the known truth. If a method works for deaths/hospitalizations (where we know the answer), we can have more confidence in its estimates for smoking and alcohol use (where we don’t).

Recontact Data

After the initial health examination closed, the FINRISK study team mailed the same questionnaire to non-participants and asked them to return it by mail (without attending the physical examination). This differs from earlier reminders – it aimed to collect at least questionnaire data on smoking, alcohol use, and other self-reported behaviors from those who wouldn’t participate fully.

An additional 473 non-participants returned the questionnaire (13% recontact response rate).

This created three distinct participation groups:

Estimates of health indicators for different participation groups.

Subset

Heavy alcohol users % (95% CI)

Daily smokers % (95% CI)

BMI ≥ 30 kg/m² % (95% CI)

Systolic blood pressure ≥ 140 mm Hg % (95% CI)

Deaths per 1,000 (95% CI)

Hospitalizations per 1,000 (95% CI)

Full cohort

—

—

—

—

33.0 (29.5–36.5)

1,157 (1,098–1,215)

Participants

5.2 (4.7–5.8)

21.8 (20.7–22.8)

21.0 (20.0–22.0)

30.7 (29.5–31.8)

22.1 (18.5–25.7)

1,052 (989–1,115)

Recontact respondents

6.4 (4.1–8.7)

33.4 (29.1–37.7)

—

—

55.1 (34.6–75.7)

1,357 (1,043–1,670)

A subset of health indicators broken down by all three participation groups. The three groups show quite different mortality and hospitalization patterns. Data from Table 5 of Karvanen et al. (2016).

Can the recontact respondents help us correct the selection bias in the participant-only estimates? To answer this, we need a formal framework for handling missing data.

A Causal Model for the Missing Data Process

Karvanen et al. (2016) built a causal model to describe the process responsible for missing responses:

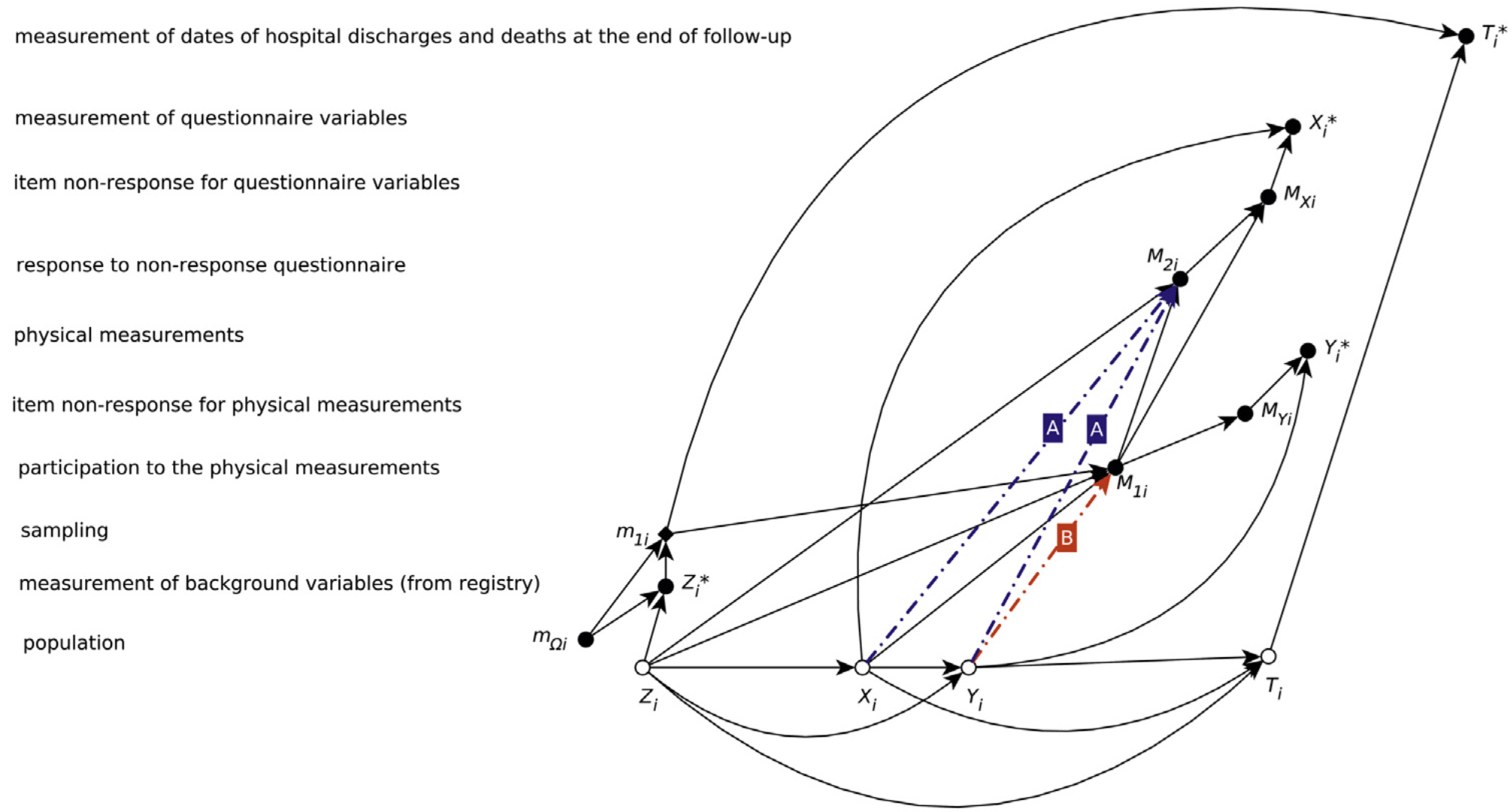

Causal model with design for the FINRISK 2007 study. Variables include background information Z, questionnaire variables X, physical measurements Y, and participation indicators M_1 and M_2. Dashed edges marked ‘A’ and ‘B’ represent assumptions about the missing data mechanism. Figure from Karvanen et al. (2016).

Legend for the causal model. Open circles are unobserved variables, filled circles are observed variables, and diamonds are indicator/decision variables. Figure from Karvanen et al. (2016).

The model includes two key assumptions:

Assumption A: Among non-participants, the recontact response is independent of unobserved health variables X and Y, conditional on background variables Z (age, sex, region). This assumption was tested empirically using follow-up data and found to hold – recontact response did not predict mortality or morbidity among non-participants when adjusted for age and sex.

Assumption B: Physical measurements Y are independent of participation M_1 given questionnaire variables X and background Z. This assumption cannot be tested with available data but is necessary for estimating prevalences of physical health indicators.

The Multiple Imputation Approach

Using these assumptions, Karvanen et al. (2016) developed a multiple imputation method tailored to this missing data mechanism (MI-MNAR).1

Checking the method: To assess whether MI-MNAR works, they compared different approaches using deaths and hospitalizations – outcomes where ground truth was available for the full cohort:

Participants-only estimates: Deaths 22.1 per 1,000 (true value: 33.0) \times

MI-MAR (assumes missing at random): Deaths 23.6 per 1,000 \times

MI-MNAR (accounts for non-random missingness): Deaths 39.8 per 1,000 (CI overlaps 33.0) \checkmark

The participants-only and MI-MAR confidence intervals failed to capture the true values, revealing systematic bias. The MI-MNAR method performed better: its confidence intervals contained the true values for both deaths and hospitalizations. While this is suggestive rather than definitive validation, it provides evidence that the modeling assumptions are reasonable.

This encouraging performance on outcomes with known truth provides some confidence for applying MI-MNAR to estimate smoking and alcohol use (where we don’t have ground truth for non-participants):

Estimates of health indicators for different participation groups and population-level estimates with three MI methods.

Subset / Method

Heavy alcohol users % (95% CI)

Daily smokers % (95% CI)

BMI ≥ 30 kg/m² % (95% CI)

Systolic blood pressure ≥ 140 mm Hg % (95% CI)

Deaths per 1,000 (95% CI)

Hospitalizations per 1,000 (95% CI)

Full cohort

—

—

—

—

33.0 (29.5–36.5)

1,157 (1,098–1,215)

Participants

5.2 (4.7–5.8)

21.8 (20.7–22.8)

21.0 (20.0–22.0)

30.7 (29.5–31.8)

22.1 (18.5–25.7)

1,052 (989–1,115)

Recontact respondents

6.4 (4.1–8.7)

33.4 (29.1–37.7)

—

—

55.1 (34.6–75.7)

1,357 (1,043–1,670)

MI-MNAR

6.8 (5.6–8.1)

27.1 (24.8–29.3)

20.8 (19.7–22.0)

29.3 (28.1–30.6)

39.8 (32.7–47.0)

1,303 (1,175–1,431)

MI-MAR

5.5 (4.8–6.3)

23.4 (22.3–24.6)

20.4 (19.3–21.6)

29.1 (27.9–30.3)

23.6 (19.7–27.5)

1,027 (968–1,085)

MI-MAR, no recontact

5.4 (4.7–6.0)

23.4 (22.3–24.6)

20.1 (19.0–21.3)

29.1 (27.9–30.2)

23.4 (19.7–27.1)

1,030 (966–1,095)

A subset of health indicator estimates using different methods. The MI-MNAR method (which properly accounts for the non-random missing data mechanism) yields estimates that differ substantially from participants-only estimates for smoking and alcohol use. Data from Table 5 of Karvanen et al. (2016).

Notice the pattern: MI-MNAR estimates for smoking (27.1%) fall between participants (21.8%) and recontact respondents (33.4%), which makes sense given that non-participants are at higher risk. For obesity, blood pressure, and cholesterol, all methods agree because the recontact questionnaire lacked good proxy questions for these physical measurements.

Key insight: Even though only 13% of non-participants responded to recontact, this data dramatically improved the estimates. The assumption that recontact respondents can proxy all non-participants (conditional on age, sex, and region) found support in the mortality and hospitalization data, where this assumption led to estimates consistent with known truth.

The Value of Recontact

The FINRISK example demonstrates that all efforts to collect data on non-participants are likely to be useful, even if the recontact response rate remains low. A 13% response rate might seem discouraging, but it provided crucial information for correcting selection bias that would otherwise remain hidden.

12.4 Types and Mechanisms of Missing Data

Missing data can be classified in two complementary ways. Understanding both perspectives is crucial for choosing appropriate analysis methods.

12.4.1 Sources of Missing Data

First, we can classify missing data by how or why they arise. There are three common sources:

Censoring: Values exceed the range of possible observations. This could be due to limitations of a physical sensor, or due to limited follow-up time (e.g., a participant is still alive at the end of a medical study, so their death date is censored).

Unobserved in random sampling: In a study asking participants to rate 10 randomly selected movies, ratings for other movies are unobserved due to the study design – a form of planned missingness.

Unobserved in non-random sampling: Among the 10 selected movies, participants may fail to rate some. This is non-random missingness that may depend on whether they’ve seen the movie, liked it, etc.

Example: Classifying Sources of Missing Data

Classify each of the following into censoring, unobserved in random sampling, or unobserved in non-random sampling:

Faulty sensors cannot record extreme values

Limited number of sensors means not all locations are monitored

Medical tests are not performed on patients who appear healthy

Survey respondents are not included because they don’t have phones

Survey participants decline to answer sensitive questions

In a movie rating study, only 10 randomly selected movies are rated per participant

In the same study, participants skip rating movies they haven’t seen

Solution

Censoring: The sensor limitation causes systematic missingness for values beyond its range.

Unobserved in random sampling: If sensor placement is random, unmonitored locations are a planned random sample.

Unobserved in non-random sampling: Decision not to test depends on health status (unobserved outcome), creating non-random missingness.

Censoring or unobserved in non-random sampling: Lack of phone creates a systematic barrier; those without phones may differ systematically from those with phones.

Unobserved in non-random sampling: Non-response to sensitive questions likely correlates with the answer itself (e.g., those engaged in sensitive behavior may be less likely to report).

Unobserved in random sampling: By design, only a random subset of movies is rated.

Unobserved in non-random sampling: Whether someone has seen a movie is not random – it relates to preferences, which likely correlate with ratings.

12.4.2 Missing Data Mechanisms (MCAR, MAR, MNAR)

The classification above describes where missing data come from (operational perspective). We now turn to a complementary classification that describes the statistical relationship between missingness and data values (analytical perspective).

The mechanism classification has three categories:

MCAR (Missing Completely at Random): Missingness is independent of all data values

MAR (Missing at Random): Missingness depends on observed values only

MNAR (Missing Not at Random): Missingness depends on unobserved values

Key Distinction: Sources vs. Mechanisms

Sources (previous section): How or why does missingness arise? (censoring, study design, selective dropout)

Mechanisms (this section): Does missingness depend on data values? If so, which ones?

These are independent classification systems. The same source can correspond to different mechanisms:

Censoring (source) can be MCAR if sensors fail randomly, or MNAR if extreme values cause failures

Non-random sampling (source) is typically MAR or MNAR depending on what drives the dropout

Understanding the mechanism (MCAR/MAR/MNAR) determines which statistical methods are valid. We now define these three mechanisms formally.

Setup and Notation

Consider a dataset Y = (Y_{\text{obs}}, Y_{\text{mis}}), where:

Y_{\text{obs}} are the observed elements

Y_{\text{mis}} are the missing elements

R denotes response indicators: R_i = 1 if element i was observed, R_i = 0 if missing

The missingness mechanism is characterized by the probability distribution p(R \mid Y) – the probability that particular values are missing, given the full data (both observed and missing parts). The missingness of Y can be divided into 3 cases:

1. Missing Completely at Random (MCAR)

Missing Completely at Random (MCAR)

Data are MCAR if p(R \mid Y) = p(R). That is, R is independent of Y – the probability of missingness doesn’t depend on any data values, observed or missing.

Examples:

A lab technician accidentally spills coffee on a random stack of patient files

Survey responses are lost in transit by postal service errors

Database corruption affects randomly selected records

2. Missing at Random (MAR)

Missing at Random (MAR)

Data are MAR if p(R \mid Y) = p(R \mid Y_{\text{obs}}). The probability of a value being missing depends only on Y_{\text{obs}} but is independent of the missing values Y_{\text{mis}} themselves.

Examples:

Urban residents are more likely to respond to online surveys than rural residents (and location is recorded)

Younger participants are less likely to respond to follow-up questionnaires (and age is known)

People with higher education levels provide more complete financial data (and education is observed)

3. Missing Not at Random (MNAR)

Missing Not at Random (MNAR)

Data are MNAR if p(R \mid Y) depends on Y_{\text{mis}} as well as possibly Y_{\text{obs}}. The probability of missingness depends on the unobserved values themselves.

Examples:

People with severe symptoms are less likely to complete a symptom severity questionnaire

Individuals with very low test scores are more likely to skip remaining test questions

Employees with poor performance ratings are less likely to complete exit surveys

Fund C in our opening example (poor performance causes dropout)

Example: Classifying Missing Data Mechanisms

An e-commerce site is recording activity data from all its customers. Which missing data mechanism applies in the following settings?

Records for a period of time are lost because a disk got full.

Software error caused activity not to be recorded for customers who used a specific payment system.

No records can be made from users of an ad-blocker.

Solution

MCAR: The disk failure is unrelated to any customer characteristics or behavior. Missingness is completely random.

MAR: Missingness depends on the payment system used, which is an observed variable (the site knows which payment system each customer uses). Once we condition on payment system, missingness is random.

MNAR: Ad-blocker usage is typically unobserved by the site (that’s the point of ad-blockers!). The missingness depends on an unmeasured characteristic that likely correlates with the user’s privacy preferences and behavior.

12.4.3 Ignorability

The key statistical question about missing data is whether the mechanism is ignorable for a particular analysis.

A missingness mechanism is ignorable if we can perform valid inference without explicitly modeling the missingness process. Whether a mechanism is ignorable depends both on the missing data mechanism (MCAR, MAR, or MNAR) and on the statistical method used.

Complete case analysis (also called listwise deletion) is the simplest approach: analyze only observations with no missing values, discarding any row with missing data. Whether this approach is valid depends on the missing data mechanism:

MCAR is ignorable for all standard methods, including complete case analysis

MAR is ignorable for likelihood-based and multiple imputation methods, but not for complete case analysis

MNAR is generally not ignorable – we must explicitly model the missingness or make strong untestable assumptions

Why does ignorability depend on both the mechanism and the

method?

MCAR: Imagine randomly tossing out some survey

responses. The remaining responses are still representative – just a

smaller random sample. Any standard analysis works fine. Complete case

analysis is safe because we’re just working with a random subsample.

MAR: Now imagine younger people are less likely to

respond, but we know everyone’s age. If we account for age properly

(e.g., by including it in our model), we can correct for the bias.

Methods like multiple imputation do this conditioning automatically. But

complete case analysis doesn’t – it just throws away the younger

non-respondents, leaving us with an unrepresentative older sample.

MNAR: Suppose people with severe symptoms are less

likely to complete a symptom questionnaire, and we don’t observe their

symptoms. There’s no variable we can condition on to fix this – the bias

is baked into what we can’t see. We must either explicitly model why

people didn’t respond (which requires strong assumptions about the

unobserved) or find auxiliary data (like the FINRISK follow-up

data).

The technical definition of ignorability involves how the likelihood

factors.

Let \(L(\theta; Y_{\text{obs}}, R)\)

be the likelihood given observed data

\(Y_{\text{obs}}\) and missingness

indicators \(R\). The joint

distribution factors as:

\[f(Y, R \mid \theta, \phi) = f(Y \mid \theta) f(R \mid Y, \phi)\]

where \(\theta\) are parameters of

interest and \(\phi\) are parameters of

the missingness mechanism.

Ignorability holds when:

The parameters \(\theta\) and

\(\phi\) are distinct

(variation in one doesn’t constrain the other)

The missingness is MAR:

\(f(R \mid Y, \phi) = f(R \mid Y_{\text{obs}}, \phi)\)

Under these conditions, we can base inference on

\(f(Y_{\text{obs}} \mid \theta)\) and

ignore

\(f(R \mid Y_{\text{obs}}, \phi)\).

For MCAR, we have even stronger ignorability:

\(f(R \mid Y, \phi) = f(R \mid \phi)\),

so missingness is completely independent of the data.

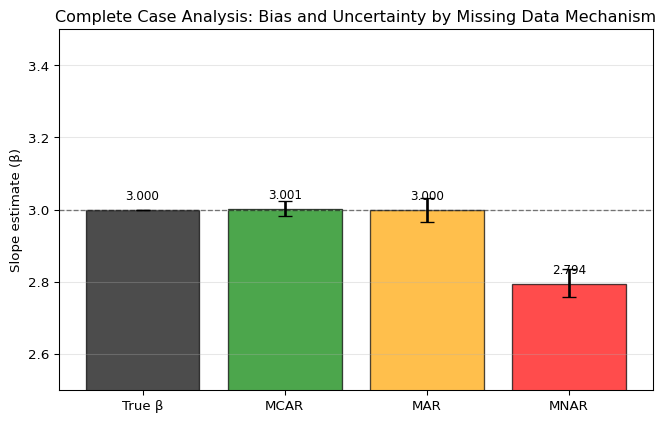

To see ignorability in action, we simulate a simple regression

problem: predicting \(y\) from

\(x\) where the true relationship is

\(y = 2 + 3x + \text{noise}\). We know

the true slope is 3.0. We then artificially impose three different

missingness patterns and see whether complete case analysis recovers the

true slope:

MCAR: Randomly delete 30% of observations

(independent of any values)

MAR: Delete observations based on

\(x\) values (higher

\(x\) → more likely to be missing)

MNAR: Delete observations based on

\(y\) values (higher

\(y\) → more likely to be missing)

Since we control the data generation, we can compare the estimated

slopes to the known truth. We repeat each scenario 100 times to assess

variability and compute 95% confidence intervals.

import numpy as npimport matplotlib.pyplot as pltfrom scipy import statsrng = np.random.default_rng(42)n =10000n_sims =100# True data generating process: y = 2 + 3x + noisetrue_beta =3.0# Three missingness mechanismsdef create_mcar_mask(x, y, rng, p=0.3):"""MCAR: Missingness independent of everything"""return rng.random(len(x)) > pdef create_mar_mask(x, y, rng):"""MAR: Missingness depends on observed x""" p =1/ (1+ np.exp(-2*x)) # Higher x => much more missingreturn rng.random(len(x)) > pdef create_mnar_mask(x, y, rng):"""MNAR: Missingness depends on unobserved y""" p =1/ (1+ np.exp(-y/1.5)) # Higher y => more missingreturn rng.random(len(x)) > p# Run simulationsresults = {'MCAR': [], 'MAR': [], 'MNAR': []}for i inrange(n_sims):# Generate data x = rng.normal(size=n) y =2+3*x + rng.normal(size=n)# Estimate under each mechanismfor name, mask_fn in [('MCAR', create_mcar_mask), ('MAR', create_mar_mask), ('MNAR', create_mnar_mask)]: mask = mask_fn(x, y, rng) slope = stats.linregress(x[mask], y[mask]).slope results[name].append(slope)# Compute means and 95% CIsmeans = [true_beta] + [np.mean(results[k]) for k in ['MCAR', 'MAR', 'MNAR']]cis = [[true_beta, true_beta]] + [np.percentile(results[k], [2.5, 97.5]) for k in ['MCAR', 'MAR', 'MNAR']]ci_lower = [means[i] - cis[i][0] for i inrange(len(means))]ci_upper = [cis[i][1] - means[i] for i inrange(len(means))]# Visualize the biasfig, ax = plt.subplots(figsize=(7, 4.5))mechanisms = ['True β', 'MCAR', 'MAR', 'MNAR']colors = ['black', 'green', 'orange', 'red']bars = ax.bar(mechanisms, means, color=colors, alpha=0.7, edgecolor='black', yerr=[ci_lower, ci_upper], capsize=5, error_kw={'linewidth': 2})ax.axhline(true_beta, color='black', linestyle='--', linewidth=1, alpha=0.5, label='True value')ax.set_ylabel('Slope estimate (β)')ax.set_title('Complete Case Analysis: Bias and Uncertainty by Missing Data Mechanism')ax.set_ylim([2.5, 3.5])# Add value labelsfor i, (bar, val) inenumerate(zip(bars, means)): height = bar.get_height() ax.text(bar.get_x() + bar.get_width()/2., height +0.02,f'{val:.3f}', ha='center', va='bottom', fontsize=9)plt.grid(True, alpha=0.3, axis='y')plt.tight_layout()plt.show()print(f"True slope: {true_beta:.3f}")for name in ['MCAR', 'MAR', 'MNAR']: mean = np.mean(results[name]) ci_low, ci_high = np.percentile(results[name], [2.5, 97.5])print(f"{name}: {mean:.3f} (95% CI: [{ci_low:.3f}, {ci_high:.3f}], bias: {mean - true_beta:+.3f})")

The simulation demonstrates key differences across mechanisms:

MCAR is unbiased – the confidence interval contains

the true value

MAR is unbiased in this specific example due to a

special case: when missingness depends only on the predictor

\(x\) in a regression, complete case

analysis for the slope coefficient happens to be unbiased.

However, this is an exception, not the rule. Complete

case analysis under MAR is biased for most estimands (means, variances,

correlations) and would be biased even for regression if missingness

depended on an auxiliary variable or if we were estimating intercepts or

predictions.

MNAR shows substantial bias because missingness

directly depends on the unobserved outcome variable

\(y\), systematically excluding high

values

Key takeaway: Complete case analysis is safe only

under MCAR. Under MAR, complete case analysis is generally biased – the

regression slope example above is a rare exception. Under MNAR, complete

case analysis is almost always biased.

The Bottom Line: Ignoring the mechanism when it’s not ignorable leads to biased results. Always assess the likely mechanism before choosing an analysis method.

Common Misunderstanding

Even if a variable is fully observed, complete case analysis can bias its estimate when missingness in other variables depends on it. Deleting rows with any missing values changes the effective sampling design.

For example, if income is fully observed but wealthy people are less likely to respond to other survey questions, complete case analysis will undersample wealthy individuals and bias the income estimate downward.

12.5 Techniques for Dealing with Missing Data

Now that we understand missing data mechanisms, we turn to methods for handling incomplete data. The appropriate method depends on the mechanism and the analysis goals.

12.5.1 Overview of Approaches

Some common ways for dealing with missing data include:

Complete case analysis (listwise deletion): Ignore entries with missing data

Imputation: Fill in the missing values with estimated values

Weighting: Reweight complete cases to represent the full sample

Model-based procedures: Build a model for the observed data that accounts for missingness

We’ll explore each of these approaches.

12.5.2 Complete Case Analysis

Complete case analysis, as we saw before, simply discards any observation with missing data and analyzes the remaining complete observations.

When appropriate: MCAR with low missingness (a common rule of thumb is < 5%, though this depends on sample size and precision requirements)

Advantages:

Simple to implement

Honest uncertainty (standard errors reflect the actual sample size)

No additional modeling assumptions

Disadvantages:

Biased under MAR/MNAR

Loss of efficiency (throwing away data)

Different analyses may use different subsets of data (if missingness patterns differ across variables)

Example: In our fund performance example, using only surviving funds is complete case analysis. It’s severely biased because missingness (fund liquidation) depends on the outcome (poor performance).

Why the “Low Missingness” Threshold?

Even when MCAR holds, complete case analysis is only recommended when missingness is low (a common rule of thumb is < 5%, though this depends on sample size and study objectives). Two key considerations:

Efficiency: Even under MCAR, discarding observations wastes data. With very low missingness, you lose minimal precision. With higher missingness (e.g., 20-40%), you’re throwing away substantial information and widening confidence intervals unnecessarily.

Assumption credibility: The MCAR assumption is harder to defend when missingness is high. If you have substantial missing data, it’s worth investing effort in methods that work under weaker assumptions (MAR).

12.5.3 Imputation Methods

Imputation refers to a class of techniques for replacing missing values with estimated values. This makes subsequent analysis easy – after imputation, we have a seemingly complete dataset.

However, imputation comes with a serious warning:

The Seduction and Danger of Imputation

The idea of imputation is both seductive and dangerous. It is seductive because it can lull the user into the pleasurable state of believing that the data are complete after all, and it is dangerous because it lumps together situations where the problem is sufficiently minor that it can be legitimately handled in this way and situations where standard estimators applied to the real and imputed data have substantial biases.

– Dempster and Rubin (1983)

Simple (Single) Imputation

Common simple imputation methods include:

Mean/median imputation: Replace missing values with the mean or median of observed values

Hot deck imputation: Randomly select a similar record and use its value

Regression prediction: Predict missing values using observed relationships

The fundamental problem with single imputation: Treating imputed values as if they were observed leads to overconfident inference. The downstream analysis method is not aware of the larger uncertainty in the imputed values.

Additional caveats:

Replacing missing values using observed values for the same variable reduces variability – estimates of variation are biased

Imputation methods based on predicting missing values may work poorly if extrapolation is needed

Mean imputation breaks relationships between variables (imputed values have zero correlation with other variables)

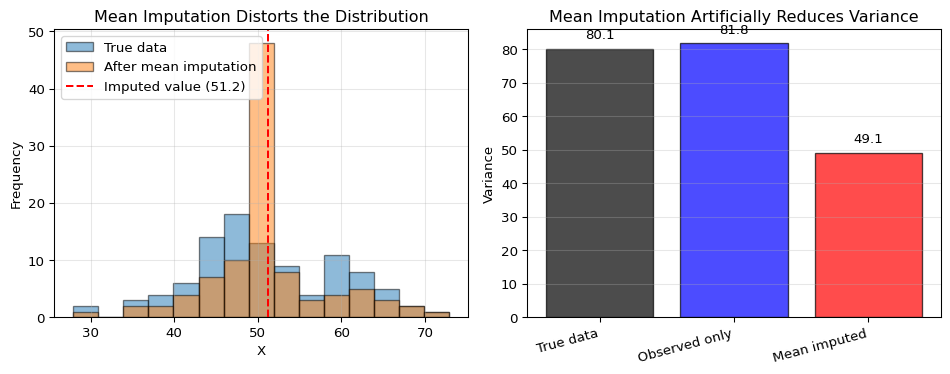

Example: How Mean Imputation Distorts Variance

To see the problem concretely, suppose we have data on a variable X with true mean 50 and standard deviation 10. We randomly make 30% of values missing (MCAR), then impute them using the sample mean. What happens to the distribution?

Variance comparison:

True data : 80.10

Observed only : 81.85

Mean imputed : 49.11

Variance reduction: 38.7%

The spike at the mean in the imputed distribution reveals the problem: all 30 imputed values are identical (the mean), while the true values would have varied. This artificially reduces variance by a substantial fraction, leading to overconfident inference – confidence intervals that are too narrow and p-values that are too small.

Multiple Imputation (MI)

Multiple imputation addresses the fundamental flaw of single imputation: treating imputed values as known. Instead of creating one “completed” dataset, MI generates multiple plausible versions (typically m = 20-50) by drawing from the distribution of possible values given the observed data. Each imputed dataset is analyzed separately using standard methods, and results are combined using Rubin’s rules2, which properly account for two sources of uncertainty: variation between imputations (uncertainty about missing values) and variation within imputations (sampling uncertainty).

Modern software packages (e.g., mice in R, IterativeImputer in Python) make implementation straightforward.

Connection to Bootstrap and Bayesian Methods

MI resembles both bootstrap and Bayesian inference:

Like bootstrap, MI generates multiple datasets and pools results to capture uncertainty

Like Bayesian methods, MI draws from a distribution of plausible values (though MI uses a frequentist framework for combining results via Rubin’s rules rather than full posterior inference)

In fact, fully Bayesian approaches to missing data are ideal but computationally intensive. MI can be viewed as an efficient approximation that works within standard frequentist workflows.

12.5.4 Weighting Methods

The idea behind weighting is to reweight the complete cases so they represent the full sample.

Inverse probability weighting (IPW):

Estimate the probability of being observed: \hat{p}_i = P(R_i = 1 \mid X_i)

Weight each complete case by w_i = 1/\hat{p}_i

Analyze weighted data

Under MAR with a correctly specified model for P(R = 1 \mid X), this gives unbiased estimates.

Example: Sex Ratio Correction in Height Estimation

Assume we wish to estimate the average height of people living in a region. We gather a sample:

70 females with average height of 166 cm

30 males with average height of 180 cm

The sample average is: \overline{X} = \frac{70 \cdot 166 + 30 \cdot 180}{100} = 170.2 \text{ cm}

However, if we know the true sex distribution is around 50:50 (not 70:30), we would get a better estimate of the population average by reweighting the group averages with the population frequencies: \overline{X}_{\text{rw}} = \frac{50 \cdot 166 + 50 \cdot 180}{100} = 173.0 \text{ cm}

This is a simple example of weighting by known population distributions.

Similar approaches are commonly used with other background variables with known population distributions: age, socioeconomic status, political preferences, etc.

12.5.5 Model-Based Procedures

Model-based procedures define a statistical model for the observed data and infer the model parameters using standard techniques (often maximum likelihood via the EM algorithm, or Bayesian methods).

Such approaches can lead to more accurate results when the incompleteness of the data is properly accounted for in the model. However:

The procedures must be adapted to deal with missing data

Existing code and tools often cannot be used as-is

The FINRISK model discussed earlier is an example of a model-based procedure – it explicitly modeled the participation process and used multiple imputation within that framework.

Advanced: Selection Models vs. Pattern-Mixture Models

When modeling MNAR data, there are two main frameworks:

Selection models (like the FINRISK approach) factor the joint distribution as: f(Y, R) = f(Y) \cdot f(R \mid Y) They model the data generating process and then the selection/missingness mechanism conditional on the data.

Pattern-mixture models take the opposite factorization: f(Y, R) = f(Y \mid R) \cdot f(R) They model the distribution of data conditional on the missingness pattern, then combine across patterns.

Both approaches require untestable assumptions about the MNAR mechanism. In practice:

Selection models are more common and intuitive but can be computationally challenging

Pattern-mixture models can be easier to specify but require careful thought about combining patterns

Sensitivity analysis is essential – vary assumptions about the MNAR mechanism and assess how conclusions change

Implementation typically requires custom likelihood functions or Bayesian modeling tools (e.g., PyMC)

12.6 Practical Implementation

12.6.1 Decision Framework

When faced with missing data, follow this workflow:

1. Assess the missingness:

How much data is missing overall?

Which variables have missing values?

Are there patterns (e.g., variables missing together)?

What is the likely mechanism (MCAR, MAR, MNAR)?

2. Choose your method:

MCAR with low missingness: Complete case analysis is acceptable (rule of thumb: < 5%, but depends on sample size and precision needs)

MCAR with higher missingness: MI for efficiency gains

MAR: MI with rich predictors (include auxiliary variables)

MNAR: Requires special methods – sensitivity analysis, auxiliary data collection (like recontact), or explicit modeling of the missingness mechanism

3. Validate your approach:

Compare observed vs. imputed distributions (imputed values should look plausible)

Perform sensitivity analyses by varying assumptions

When possible, check against external data (like the FINRISK follow-up data)

Compare MI-MAR vs. MI-MNAR results to understand the impact of MNAR assumptions

Reporting Guidelines

Transparency is essential when dealing with missing data. A complete report should include:

Amount and pattern of missingness: Report overall percentage and range across variables

Assumed mechanism and justification: State whether you assume MCAR, MAR, or MNAR and why

Method used: Specify whether you used complete case, MI, weighting, or model-based methods

Implementation details:

For MI: number of imputations, imputation models, predictors used

For weighting: how weights were estimated

Software and packages used

Sensitivity analyses: Report results under different assumptions

Impact assessment: Describe how results differ from complete case analysis

12.6.2 Prevention is Better than Correction

The best way to handle missing data is to prevent it. A researcher can design data collection to minimize missingness:

Shorter surveys with clear, relevant questions (reduces respondent fatigue)

Incentives for completion (monetary, results reports, lottery entries)

Follow-up protocols for non-respondents (like FINRISK’s recontact approach)

Pilot testing to identify problematic questions before full deployment

Collect auxiliary data for non-respondents when possible – even limited data can dramatically improve estimates

The FINRISK example demonstrated that even a 13% recontact response rate provided crucial information for correcting selection bias. All efforts to collect data on non-participants are worthwhile.

When Standard Methods Fail

Be aware of situations where even proper methods struggle:

Very high missingness (> 40%): Results become increasingly dependent on modeling assumptions rather than data

MNAR without auxiliary information: No method can reliably recover the truth without strong, untestable assumptions about the missingness mechanism

Extrapolation beyond observed data: Imputation requiring predictions far outside the range of observed values is inherently unreliable

Fundamental limitation: No statistical method can recover information that isn’t there. If the missing data mechanism is MNAR and you have no auxiliary information about non-respondents, your estimates will be biased. The best you can do is acknowledge the limitation explicitly, perform sensitivity analyses showing results under different assumptions, and discuss the likely direction and magnitude of bias.

12.7 Chapter Summary and Connections

12.7.1 Key Concepts Review

Two classification systems:

Sources (how missingness arises): Censoring, random sampling, non-random sampling

Mechanisms (statistical relationship): MCAR, MAR, MNAR

Missing data mechanisms:

MCAR (Missing Completely at Random): Missingness independent of all data

MAR (Missing at Random): Missingness depends only on observed data

MNAR (Missing Not at Random): Missingness depends on unobserved values

Ignorability:

MCAR: Ignorable for all methods (complete case analysis is unbiased)

MAR: Ignorable for likelihood-based and MI methods, but NOT for complete case analysis

MNAR: Generally not ignorable – requires explicit modeling or auxiliary data

Key methods:

Complete case analysis: Only valid under MCAR with low missingness

Multiple imputation: The workhorse for MAR; generates m datasets, analyzes each, pools with Rubin’s rules

Weighting: Reweight complete cases to represent full sample (inverse probability weighting)

Model-based procedures: Explicitly model the missingness mechanism

Real-world impact:

Survivorship bias (investment funds): Using only surviving funds systematically overstates returns, misleading billions in investment decisions

Selection bias (FINRISK): Non-participants had substantially higher mortality; ignoring them produces dangerously wrong public health estimates of smoking and alcohol use

12.7.2 The Big Picture

Missing data is not a niche technical problem – it’s a fundamental challenge in real-world data analysis that affects investment decisions, public health policy, and life-and-death medical outcomes.

We have principled methods for handling missing data, but they require careful thought and honest assessment. The key: understand the missingness mechanism, choose methods accordingly, validate assumptions when possible, and report transparently about limitations. No statistical method can compensate for very high missingness or MNAR without auxiliary data – prevention and auxiliary data collection (like FINRISK’s recontact effort) are invaluable.

12.7.3 Common Pitfalls to Avoid

Assuming MCAR without evidence: Most real-world missing data are not MCAR. Compare complete vs. incomplete cases before assuming missingness is random.

Naïve imputation: Mean imputation destroys variance; single imputation understates uncertainty. Use proper multiple imputation.

Ignoring auxiliary information: Include variables that predict missingness in imputation models, even if they’re not in your analysis model. The FINRISK recontact data – just 13% response – dramatically improved estimates.

Hiding your assumptions: Document your missingness mechanism assumptions, methods used, and sensitivity analyses. Readers cannot judge validity without this transparency.

Misspecified models and false confidence: Imputation models can introduce bias if misspecified. When MNAR is plausible but you use MAR methods, your uncertainty is understated. Validate and conduct sensitivity analyses.

12.7.4 Chapter Connections

Previous (Chapters 5-11):

Chapters 5-7 developed parametric inference, estimation, and hypothesis testing – all assuming complete data. Missing data violates this assumption and can bias estimates, widen confidence intervals artificially (mean imputation), or lead to invalid p-values

Chapter 9’s regression methods are vulnerable to selection bias when missingness depends on outcomes (like Fund C’s poor performance leading to dropout) – complete case analysis can severely bias coefficient estimates

Chapter 11’s causal inference framework helps understand missing data mechanisms – whether missingness depends on observed vs. unobserved variables determines if we can recover valid estimates

This Chapter: Addressed missing data through three mechanisms (MCAR, MAR, MNAR) and their appropriate methods. We saw how survivorship and selection bias can severely distort inference, and learned when complete case analysis fails versus when multiple imputation or model-based approaches are needed.

Next (Ch. 13):

Chapter 13 (Experimental Design and Surveys) will show how proper study design minimizes missingness and enables causal inference – the principles here inform power calculations, sample size planning, and follow-up protocols to reduce missing data

12.7.5 Self-Test Problems

Mechanism Classification: For each scenario, identify whether the missing data are MCAR, MAR, or MNAR:

A thermometer fails to record temperatures below -20°C due to physical limitations

Survey respondents from rural areas are less likely to complete an online survey (and location is recorded)

People with high anxiety scores are less likely to complete an anxiety questionnaire (and anxiety is what we’re measuring)

Solution

Source: Censoring (instrument lower limit). Mechanism: MNAR, because the probability of missingness depends on the unobserved value itself (temperatures below −20°C are deterministically missing).

Mechanism: MAR. Missingness depends on location, which is observed; conditional on location, response is random.

Mechanism: MNAR. Missingness depends on the unobserved anxiety score itself.

Survivorship Bias Calculation: Suppose a database contains 100 funds at year 0. After 5 years, 60 funds survive. The surviving funds show an average return of 8% per year. If the 40 defunct funds had an average return of -2% per year, what is the survivorship bias?

This is even larger than the hedge fund bias estimated by Fung & Hsieh! If instant history bias adds +1.4% per year, the combined bias would be 5.4% per year.

Complete Case Bias: Assume income and health are positively correlated. A study measures income (fully observed) and health status (missing for 30% of respondents). Healthier people are more likely to respond. Will complete case analysis bias the income estimate? Why or why not?

Solution

Yes, complete case analysis will bias the income estimate even though income is fully observed. Since health and income are positively correlated (e.g., healthier people have higher income due to employment), the complete cases will oversample healthier individuals and thus oversample higher-income individuals. Deleting rows changes the effective sampling design, biasing estimates even for fully observed variables.

Ignorability and Valid Methods: Fill in which methods produce valid inference without explicitly modeling the missingness mechanism:

Mechanism

Complete Case Analysis

Likelihood/ML Methods

Multiple Imputation

MCAR

?

?

?

MAR

?

?

?

MNAR

?

?

?

Solution

Mechanism

Complete Case Analysis

Likelihood/ML Methods

Multiple Imputation

MCAR

\checkmark

\checkmark

\checkmark

MAR

\times

\checkmark

\checkmark

MNAR

\times

\times*

\times*

*MNAR requires explicitly modeling the missingness mechanism or bringing auxiliary data/assumptions (selection models, pattern-mixture models, sensitivity analyses).

Method Selection (True/False):

With 3% missing data and MCAR, complete case analysis is acceptable.

With 30% missing data and MAR, complete case analysis is generally unbiased.

With plausible MNAR and no auxiliary information, sensitivity analysis is essential.

Solution

True - Under MCAR with low missingness (rule of thumb: < 5%), complete case analysis is valid though less efficient.

False - Even under MAR, complete case analysis is biased. The high missingness (30%) makes efficiency loss severe, but MAR methods like multiple imputation are needed for validity.

True - With MNAR and no auxiliary data, results are sensitive to untestable assumptions. Sensitivity analysis showing results under different MNAR assumptions is essential for honest inference.

# Multiple Imputation with statsmodels MICE (imputation + pooling handled internally)import pandas as pd# Quick missingness checkdf.isnull().sum() # per-column countsdf.isnull().sum().sum() / df.size # overall proportionimport statsmodels.api as smfrom statsmodels.imputation.mice import MICEData, MICE# df: your pandas DataFrame with missing valuesmd = MICEData(df) # chained equations setup# Specify analysis modelmodel = sm.OLS.from_formula('y ~ x1 + x2', md)# Fit with multiple imputations; pooled inference returnedres = MICE(model, md, n_imputations=50, model_class=sm.OLS).fit()# res.summary() # pooled estimates and standard errors

Other Python options include

sklearn.impute.IterativeImputer and miceforest

(random forest-based).

library(mice)# Quick look at missingnesssummary(df)md.pattern(df)# Multiple Imputation with poolingimp <-mice(data = df,m =50, # number of imputationsmethod ="pmm", # predictive mean matching for continuous varsseed =123)fit <-with(imp, lm(y ~ x1 + x2))pooled <-pool(fit)summary(pooled)# Access a completed dataset if needed:# complete(imp, action = 1) # first imputation# complete(imp, action = "long") # all imputations in long format

Other R packages include Amelia and mi.

12.7.7 Connections to Source Material

This chapter synthesized material from multiple sources. The theoretical framework for missing data mechanisms (MCAR, MAR, MNAR) and ignorability follows Little & Rubin’s foundational Statistical Analysis with Missing Data. Two key empirical studies demonstrated real-world impact: Fung and Hsieh (2000) quantified survivorship and instant history bias in hedge fund databases, while Karvanen et al. (2016) demonstrated selection bias correction in the FINRISK health survey using multiple imputation for MNAR data.

12.7.8 Further Reading

Foundational Text: Little, R. J. A., & Rubin, D. B. (2019). Statistical Analysis with Missing Data (3rd ed.). Wiley.

Practical Guide: Van Buuren, S. (2018). Flexible Imputation of Missing Data (2nd ed.). CRC Press. Free online

Case Studies: The papers by Fung and Hsieh (2000) and Karvanen et al. (2016) provide excellent examples of missing data in practice.

Remember: Missing data is not just a technical nuisance – it’s a fundamental challenge that can determine whether your analysis leads to valid conclusions or serious errors. Understand the mechanism, choose methods appropriately, and always report your approach transparently!

Fung, William, and David A Hsieh. 2000. “Performance Characteristics of Hedge Funds and Commodity Funds: Natural Vs. Spurious Biases.”Journal of Financial and Quantitative Analysis 35 (3): 291–307.

Karvanen, Juha, Hanna Tolonen, Tommi Härkänen, Pekka Jousilahti, and Kari Kuulasmaa. 2016. “Selection Bias Was Reduced by Recontacting Nonparticipants.”Journal of Clinical Epidemiology 76: 209–17.

MI-MNAR = Multiple Imputation for data Missing Not at Random.↩︎

Rubin’s rules provide formulas for combining point estimates and variances from multiple imputed datasets. The total variance accounts for both within-imputation uncertainty (sampling variability) and between-imputation uncertainty (uncertainty about the missing values).↩︎

Model misspecification means using a model that doesn’t match the true data-generating process – e.g., assuming linearity when the relationship is nonlinear, or assuming independence when variables are correlated.↩︎

Source Code